- Services

- Industries

- Expert Centre

- CRUX

- Events

- News & Insights

- About Us

- Join Us

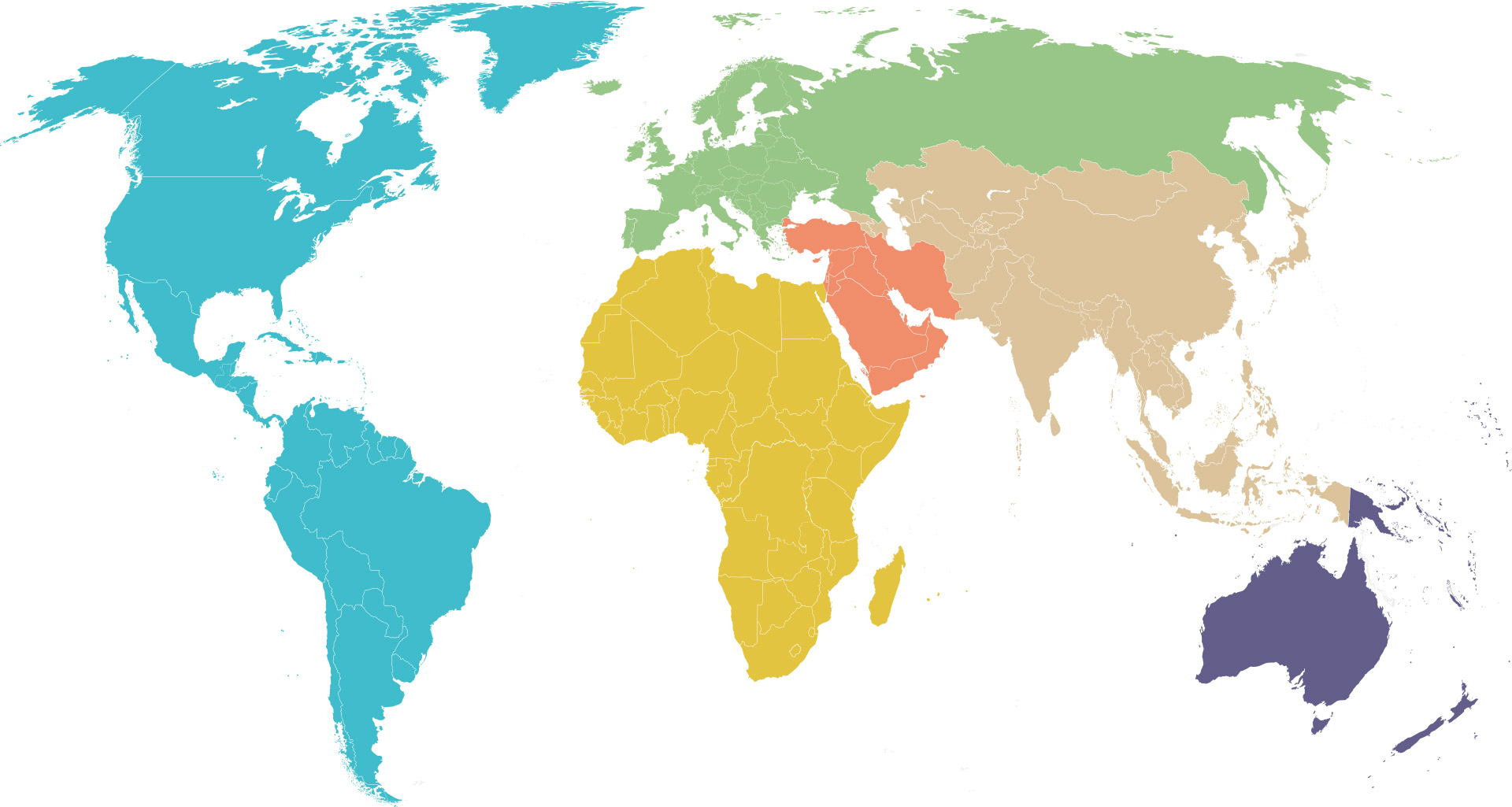

442

projects

18

countries

$1.08bn

average CAPEX value

$61.5m

average value claimed

61.2%

average EOT claimed

32

projects

15

countries

$1.87bn

average CAPEX value

$104m

average value claimed

83.7%

average EOT claimed

329

projects

12

countries

$1.98bn

average CAPEX value

$134m

average value claimed

84.7%

average EOT claimed

93

projects

21

countries

$6.43bn

average CAPEX value

$93.5m

average value claimed

64.4%

average EOT claimed

122

projects

4

countries

$3.52bn

average CAPEX value

$90.3m

average value claimed

78.1%

average EOT claimed

383

projects

24

countries

$689m

average CAPEX value

$136m

average value claimed

64.0%

average EOT claimed

COVID has unilaterally stalled the movement of people and goods within and between regions, slowed production of materials and products, altered conditions for workers, imposed new constraints, and negatively impacted the industry’s productivity. Employers and contractors are experiencing increased project delays and disruption, cost overruns, and divergence from business case estimates.

Over the last decade, many international organisations delivering capital projects have come to rely on highly mobile personnel and labour. This trend was enabled by cheaper travel, legislative environments allowing freedom of movement, and expansion of recruitment and supply channels across and between continents.

The pandemic, along with international variations in vaccination levels and requirements, has raised barriers. High demand is also exposing scarcity in human resources, particularly in developed economies where the construction and engineering industry is unable to attract sufficient new blood to replenish its ageing workforce.

To drive efficiency and eliminate waste, many organisations have adopted lean production principles, such as Total Quality Management, and just-in-time logistics, whose successful operation is dependent on the use of complex, international supply chains. Operating in this way not only requires investment in supporting systems,

but also intensive planning and scheduling, and detailed awareness of strategic risk. Before the pandemic, the prospect of such a shock to the global economy and capital project ecosystem was not on the risk management radar or catered for in standard forms or bespoke construction contracts.

One positive impact of the COVID crisis has been the accelerated adoption of digital communications and technologies. This has not only enabled remote working but has afforded projects access to a wider talent pool, with a potentially global reach for certain skills. Digital models, drones, robotics, virtual / augmented reality, and other advanced systems have also found new advocates and applications in a traditionally conservative industry.

However, most of the benefits from technology have been seen in management, planning and design, modelling and professional services.

Other parts of the construction process have slowed the pace of project delivery due to bottlenecks in logistics, stock, sequencing, and on-site labour. Also, the use of BIM is often not sufficiently comprehensive, understood or supported to realise its full potential. The lagging productivity of the construction and engineering industry is largely due to sluggish adoption of technology and resistance to change.

Many Governments see investment in infrastructure as a viable method of stimulating their economies. As well as the short-term benefits in trading activity and jobs, there are longerterm gains in terms of connectivity, business productivity, community services, revenue streams, and asset portfolios with enhanced environmental performance. However, a bow wave of largescale projects being let to the market requires careful management, execution, and integration with other developments if value for money is to be achieved. This combination of well-planned activity and a properly structured pipeline – that can be relied on by the supply chain – is essential to ensure that demand can be met without overstretching the industry or overheating the market.

From Germany and Belgium to Australia, and from North America to India, flash floods, forest fires and other extreme weather events have borne out the increasingly stark warnings of the international scientific community. The increase in gas and oil prices is forcing companies and organisations of all sorts to recalibrate their energy budgets and usage. Pressure is increasing for government and regulatory intervention to promote sustainability in all sectors, not least construction and the built environment.